The public was introduced to Open AI's ChatGPT on November 30, 2022. It took a month for the potential of this breakthrough to electrify the performance of tech stocks. The tech sector in the S&P500, measured by the XLK ETF, dropped in December. But XLK took off at the beginning of January and returned 55% in 2023.

Even though ChatGPT amazed investors, there were questions in December 2022 about the profit opportunity in AI. In early January, there were several media reports and speculations about Microsoft's potential investment in OpenAI. On January 23, 2023, Microsoft announced a massive investment in the company. The turnaround for tech stocks in January was likely the market's reaction to Microsoft's explicit endorsement of AI as a commercial opportunity.

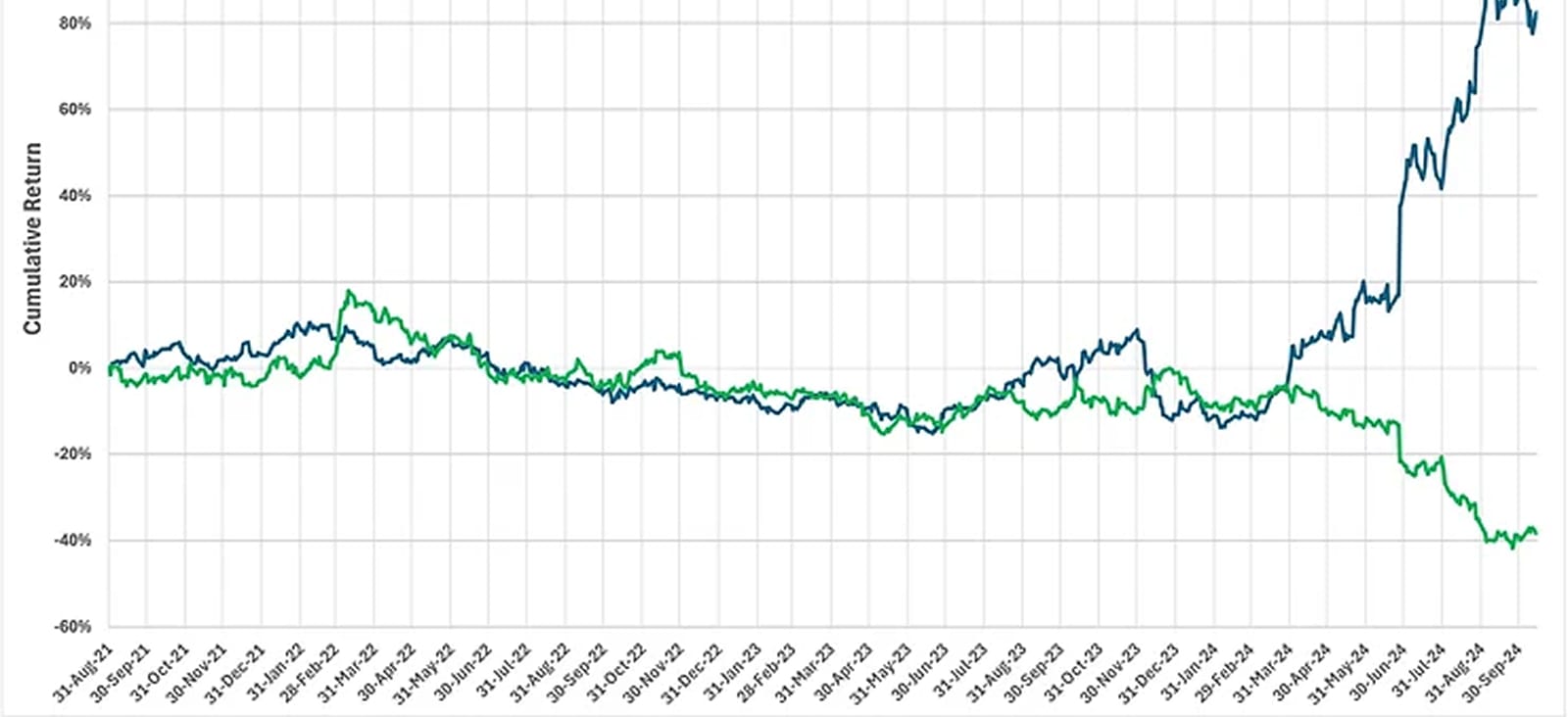

Microsoft's investment raised the question of who the winners in AI would be besides Microsoft and NVIDIA. It appears that investors answered that the best bet was that it would likely be among tech companies that spend the most on R&D. This inference is prompted by the behavior of a monthly rebalanced long-short portfolio of stocks in the tech sector of the S&P500 that is long the companies with the highest R&D spending divided by sales and short the companies with the lowest R&D/Sales. The chart shows the three-year cumulative return of the R&D/Sales factor. The chart also includes the cumulative return of two long-short quality factors, ROE and ROIC.

The R&D/Sales long-short factor took off at the beginning of January, returning 47% in 2023 with a 4.5 information ratio. In 2023, ROE in tech stocks lost 6%, while ROIC returned 10%. The quality factors help explain the observation on the chart's right that R&D/Sales as a factor in Tech has not performed well since early April 2024. However, ROE as a long-short factor bottomed in March. And ROIC has returned 14% since the end of April. Quality has performed well in tech stocks over the past few months as R&D/Sales has lost steam.

A simple interpretation is that questions about the extent of the profit opportunity in AI have resurfaced. There has been a rotation from potential tech innovators, indicated by their R&D spending relative to sales, to quality tech companies. The AI investing frenzy of 2023 seems to have morphed into AI fatigue.