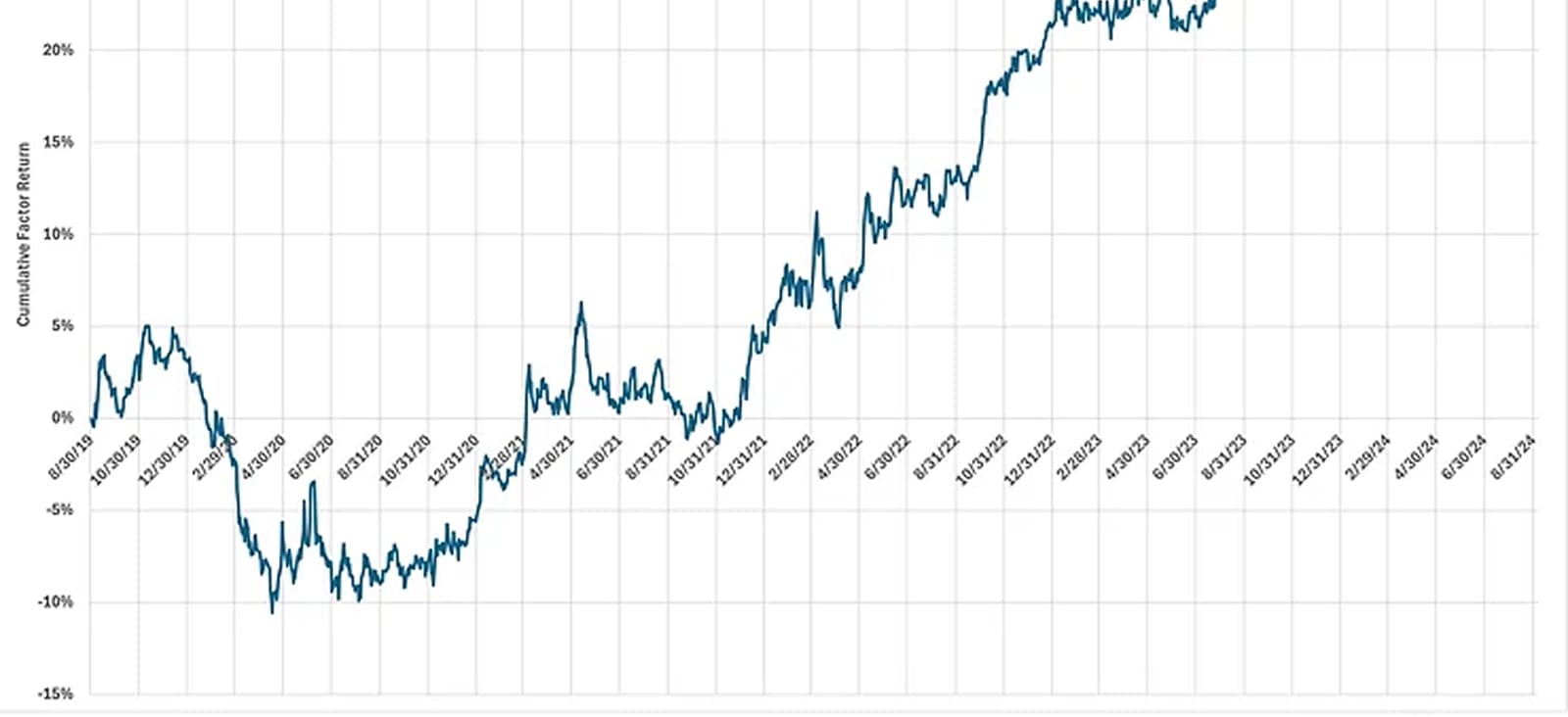

It is surprising and potentially alarming that financial leverage has been a powerful driver of stock returns during the market rally over the past year.

The sales/employee ratio should be a good measure of employee productivity. However, it varies considerably across market sectors, much higher in capital-intensive industries such as energy and utilities and much lower in more labor-intensive sectors such as industrials and consumer discretionary.

In his March State of the Union address, President Biden proposed raising the excise tax on stock buybacks from 1% to 4% to discourage companies from engaging in stock repurchases. On April 12, the Department of Treasury and the IRS followed up with proposed regulations on stock buybacks.

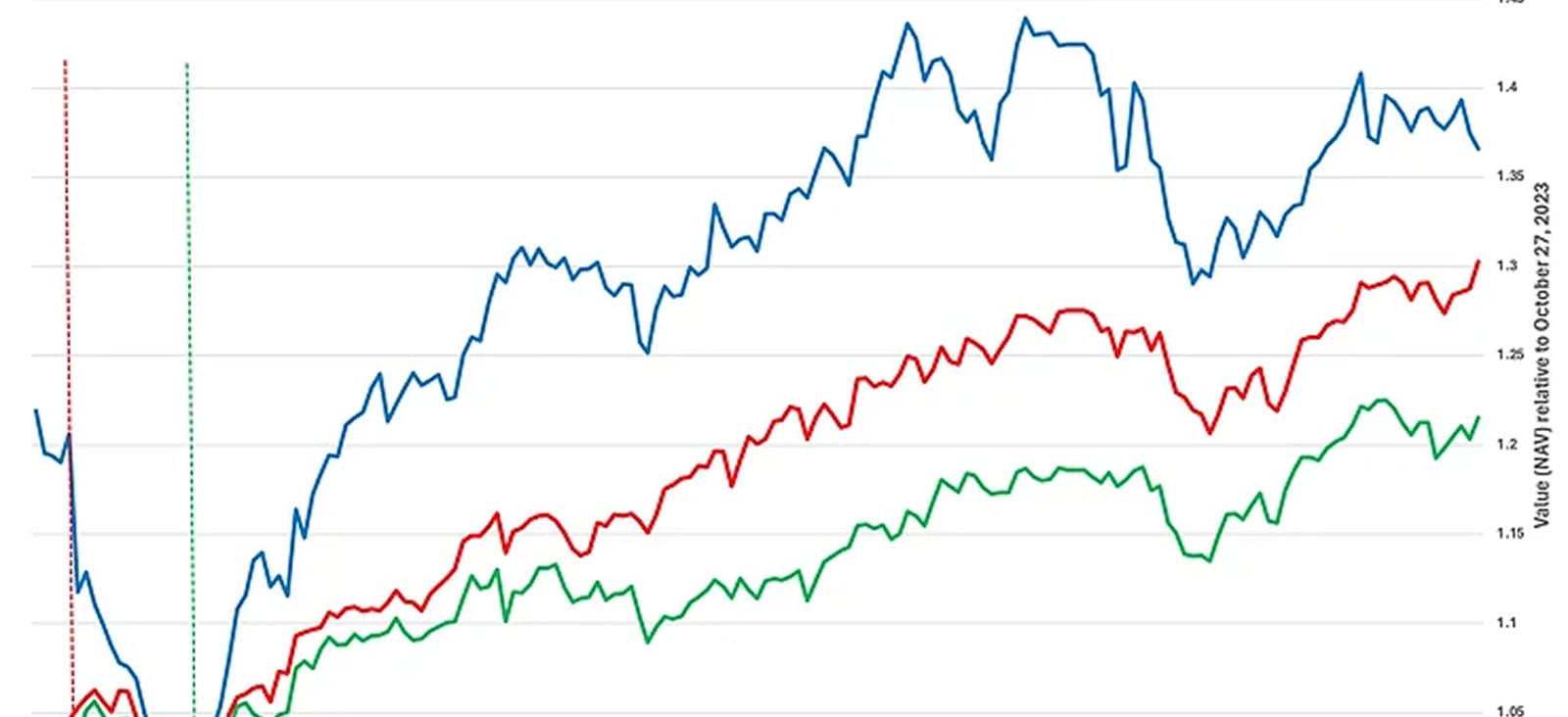

Momentum was a driving force for the market in 2024 until momentum peaked on July 9. Momentum resumed its upward climb at the end of July, and the question now is whether momentum will continue to be a force, perhaps driving the market upward as it did before the summer.

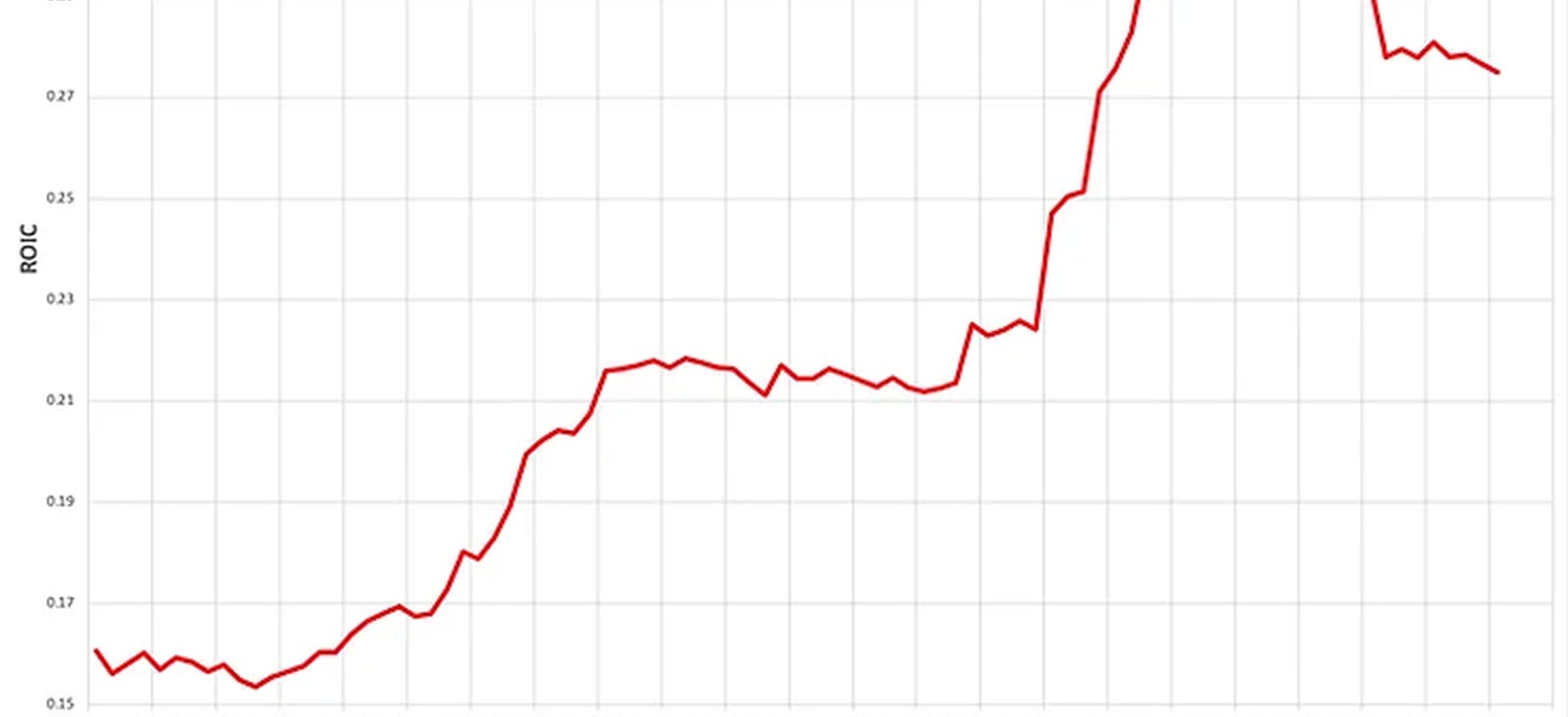

A distinction of tech companies is that they are sources of innovation and growth. In addition, large-cap tech companies often rank among the highest quality in the market when evaluated by typical measures such as Return on Equity (ROE).

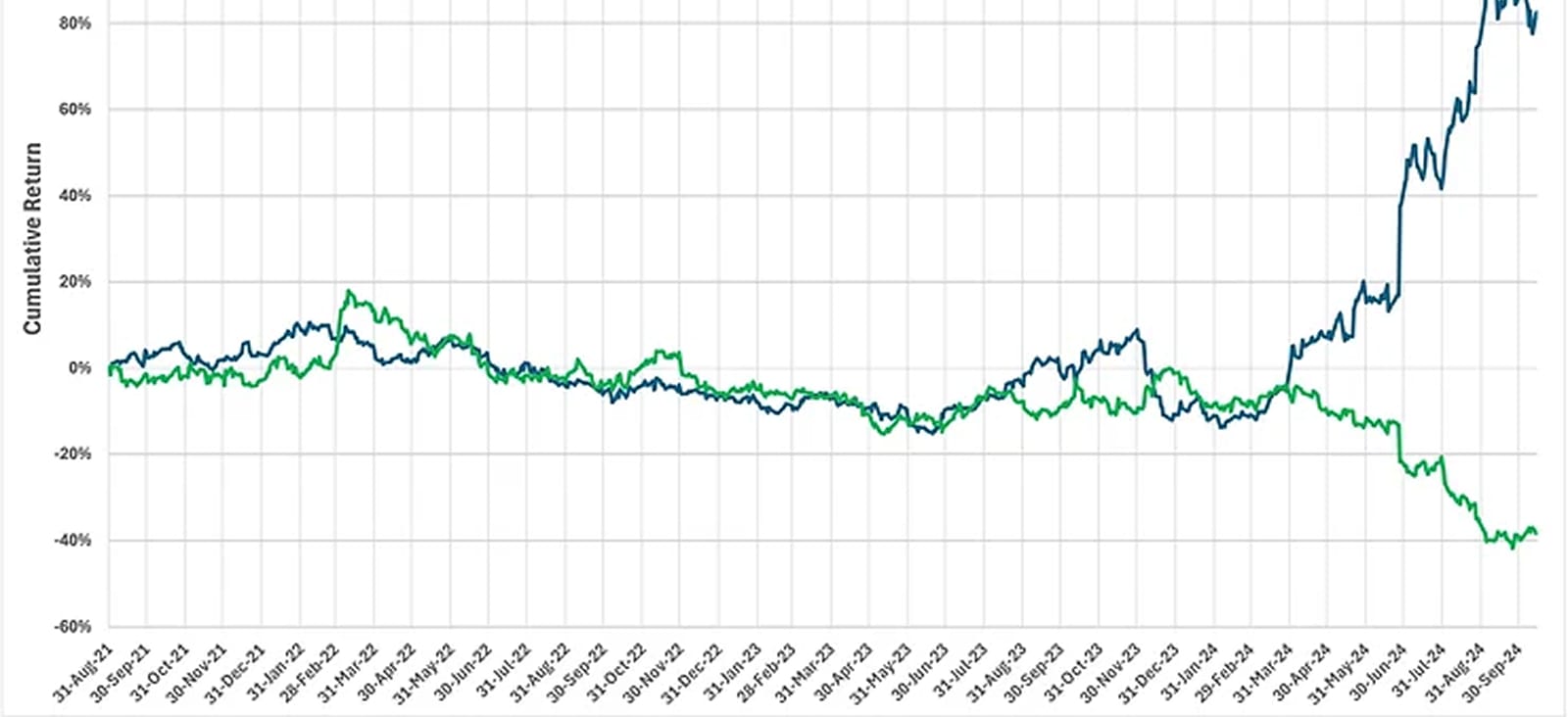

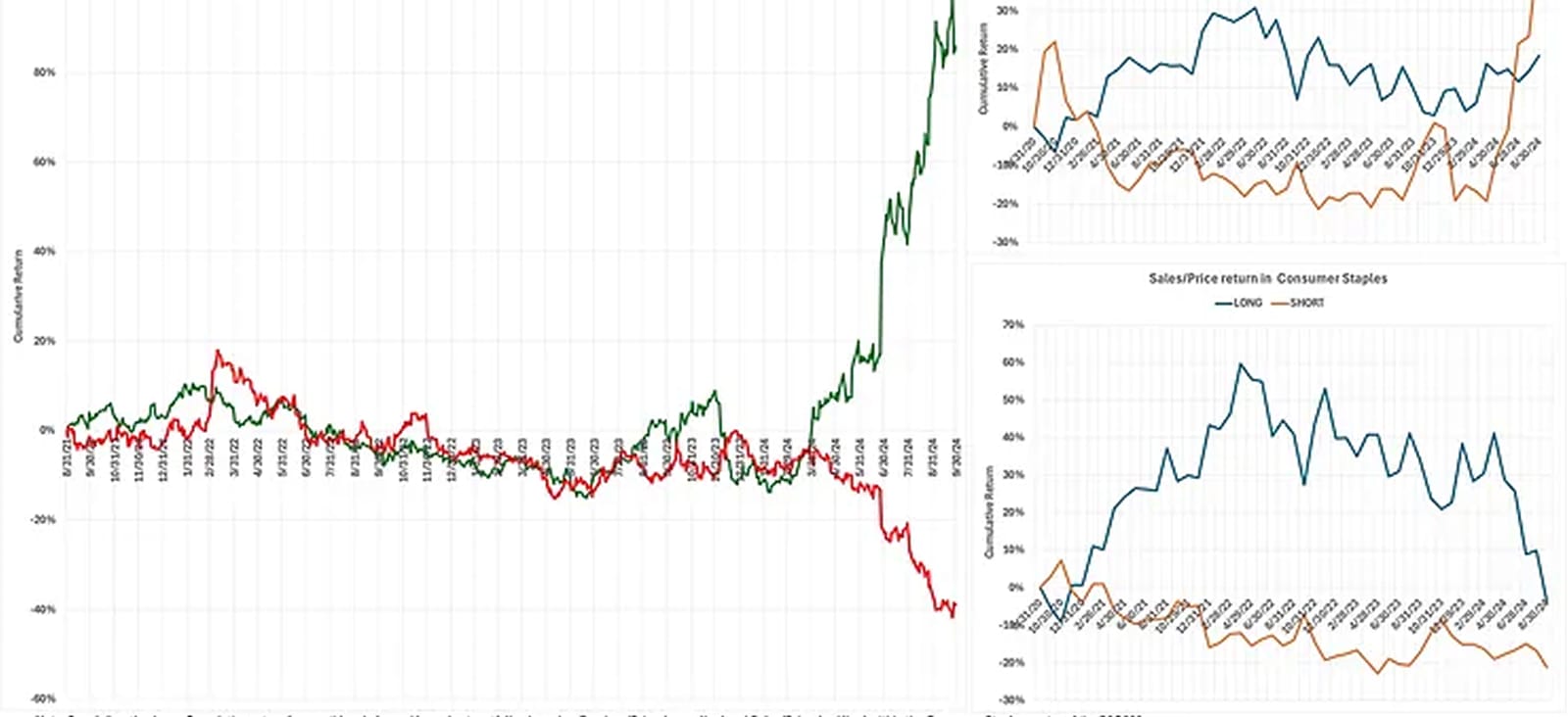

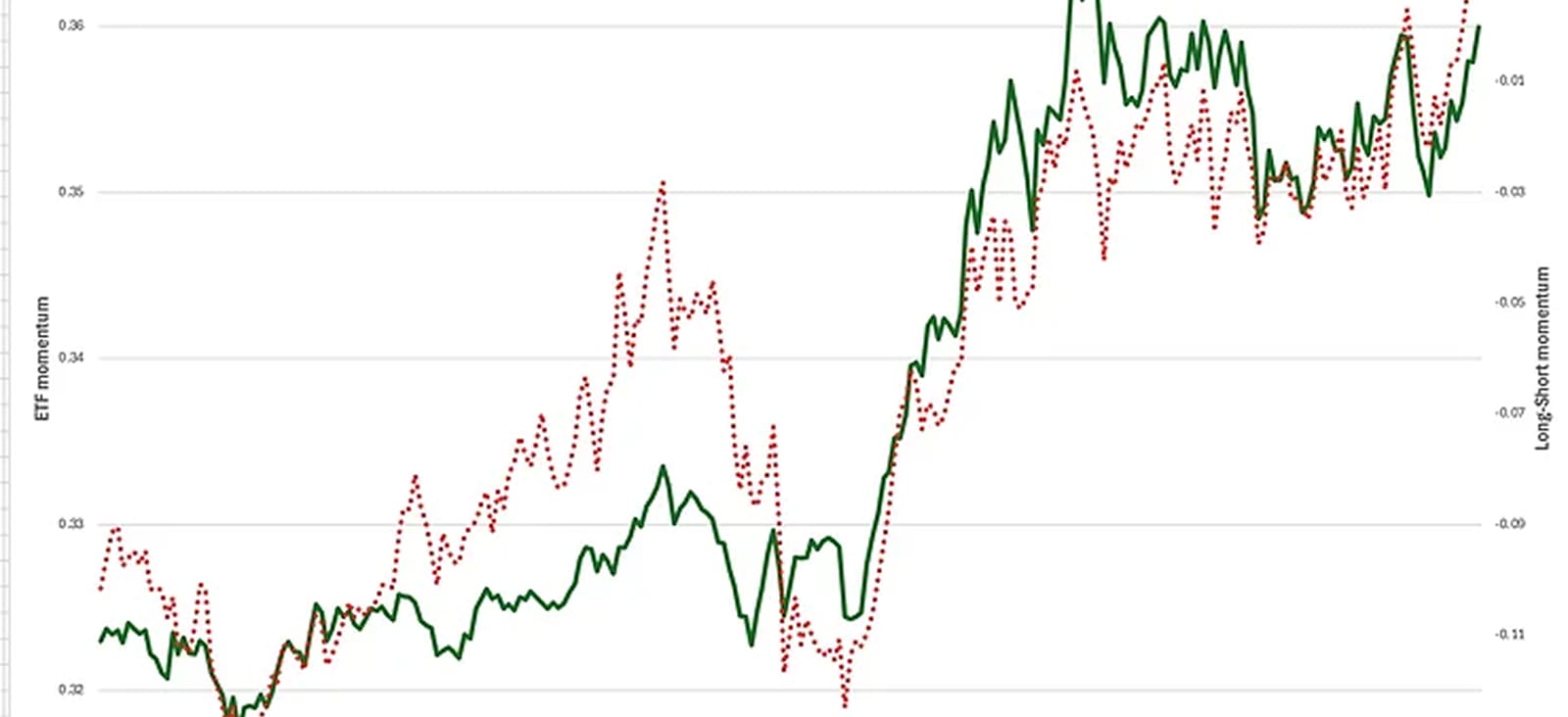

Two notable features of the 2024 market rally were the power of momentum and the dominance of large-cap stocks. The market peaked on July 16, but momentum and size peaked a week earlier, on July 9.

The public was introduced to Open AI's ChatGPT on November 30, 2022. It took a month for the potential of this breakthrough to electrify the performance of tech stocks. The tech sector in the S&P500, measured by the XLK ETF, dropped in December.

The S&P500 has returned 15% through June 20, 2024. Half of the gains were achieved since early May. Momentum also has a strong 2024, but its excess return this year was achieved before early March. Since then, the power of momentum has spread throughout the market.

It took eight weeks after the 9/11 attack on the US for the S&P500 to sustain its recovery to its pre-9/11 level. The rebound from its 9/21 low was substantial, returning 21% by mid-March.

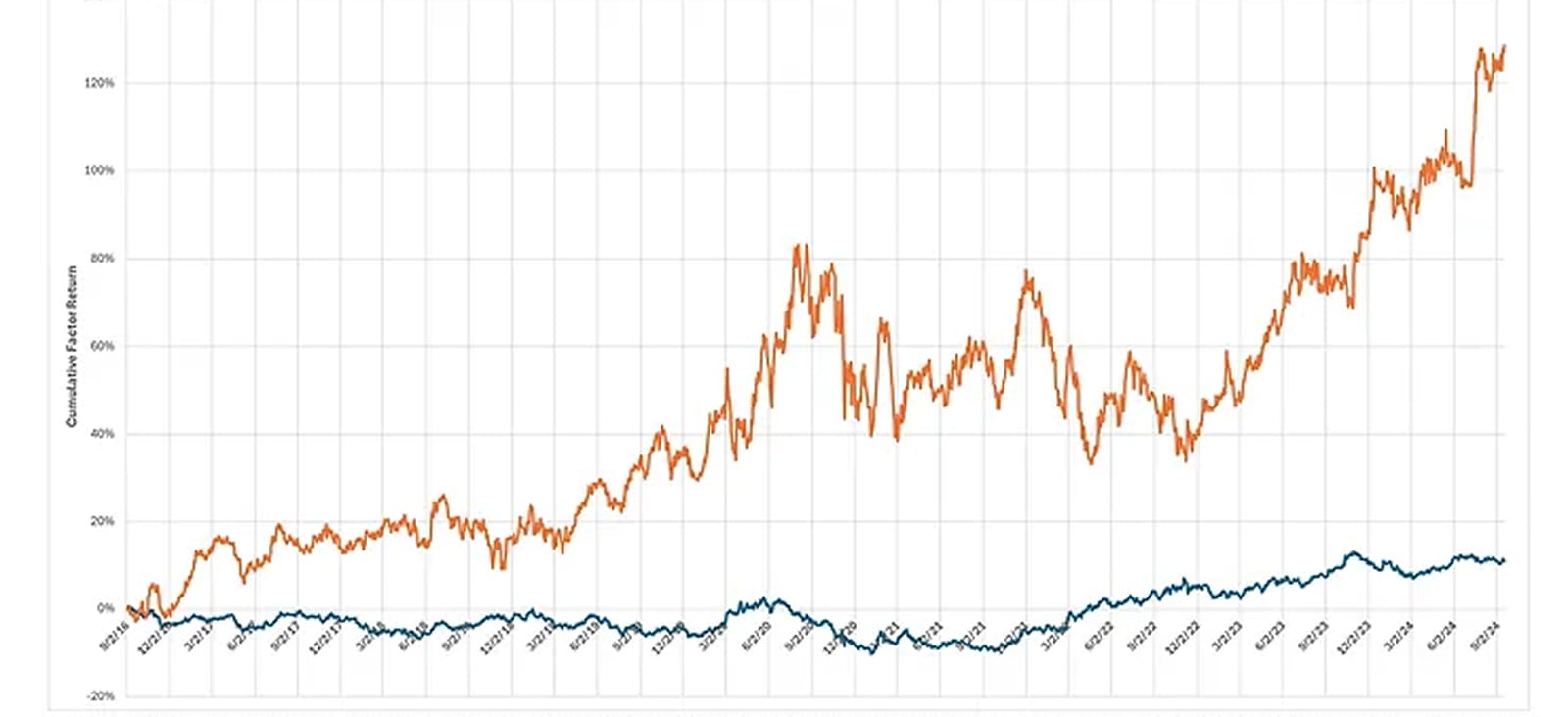

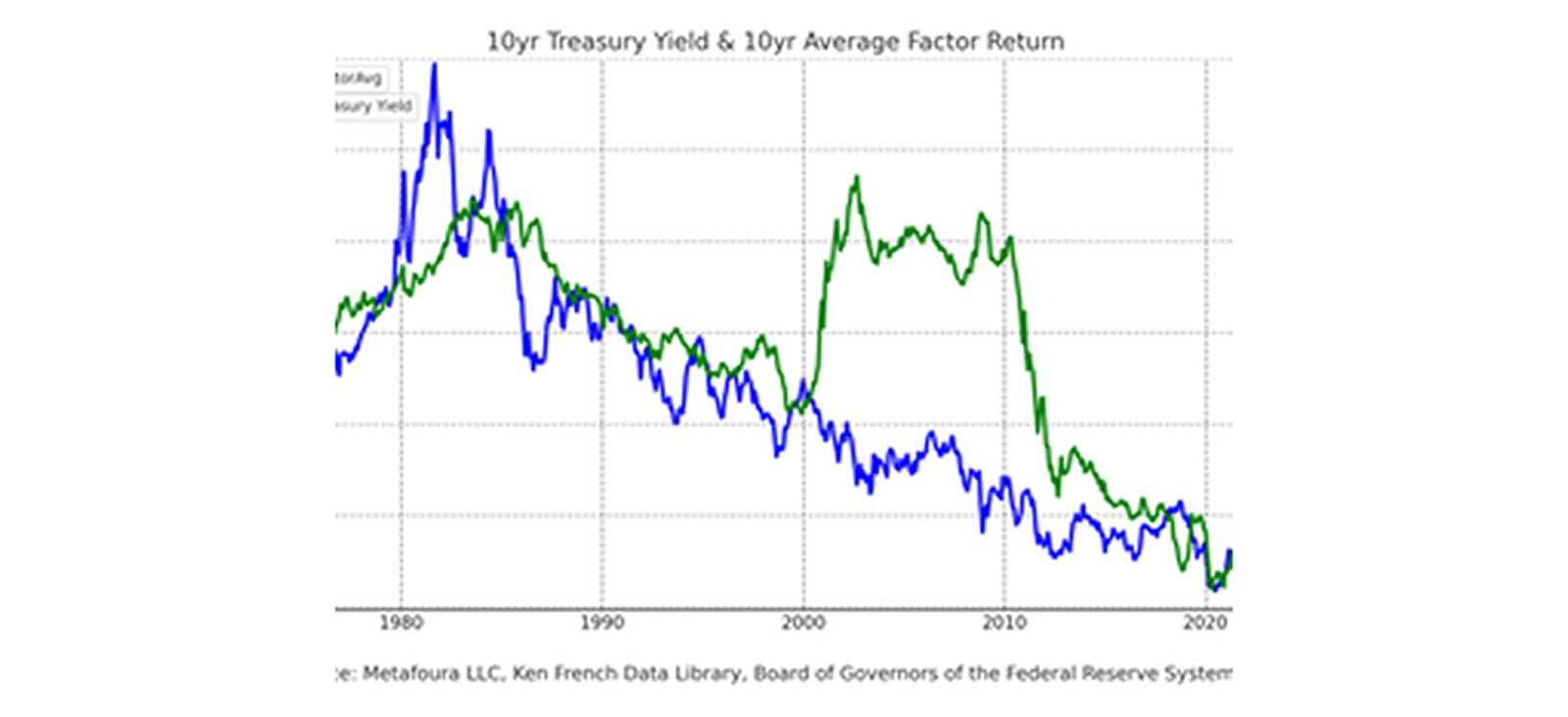

In previous articles, I've highlighted the strong correlation between the direction of bond yields and the return to Free Cash Flow yield (FCF yield - Free Cash Flow per share divided by current share price).

The markets are frustrated, waiting for a decline in interest rates. There is now the added concern of rates going higher. In a recent note, I showed that when credit risk is tight, as it is now, FCF yield (Free Cash Flow per share divided by current share price) moves in tandem with...

Except for a few days in 2005, the spread between corporate and treasury bond yields hasn’t been as low as it is now since 1997. These low credit spreads are the backdrop for the pivotal role of treasury yields in the US contest between growth and value stocks.

The problem with ESG is that this label bolts together three different topics: Environmental, Social, and Governance. The ESG label was introduced and made mainstream in the 2004 United Nations Report ‘Who Cares Wins.’

Recently, I posted about using large language models of AI to analyze earnings calls for sentiment to pick stocks. In addition to sentiment, these models can also rank the importance of the various themes extracted from the earnings call.

Ask Chat GPT a question, and it will give you an answer. We're all familiar now with the incredible power of large language models to harvest the content on the internet to provide us with answers to complex questions. ChatGPT-4 is extraordinary for summarizing and suggesting things.

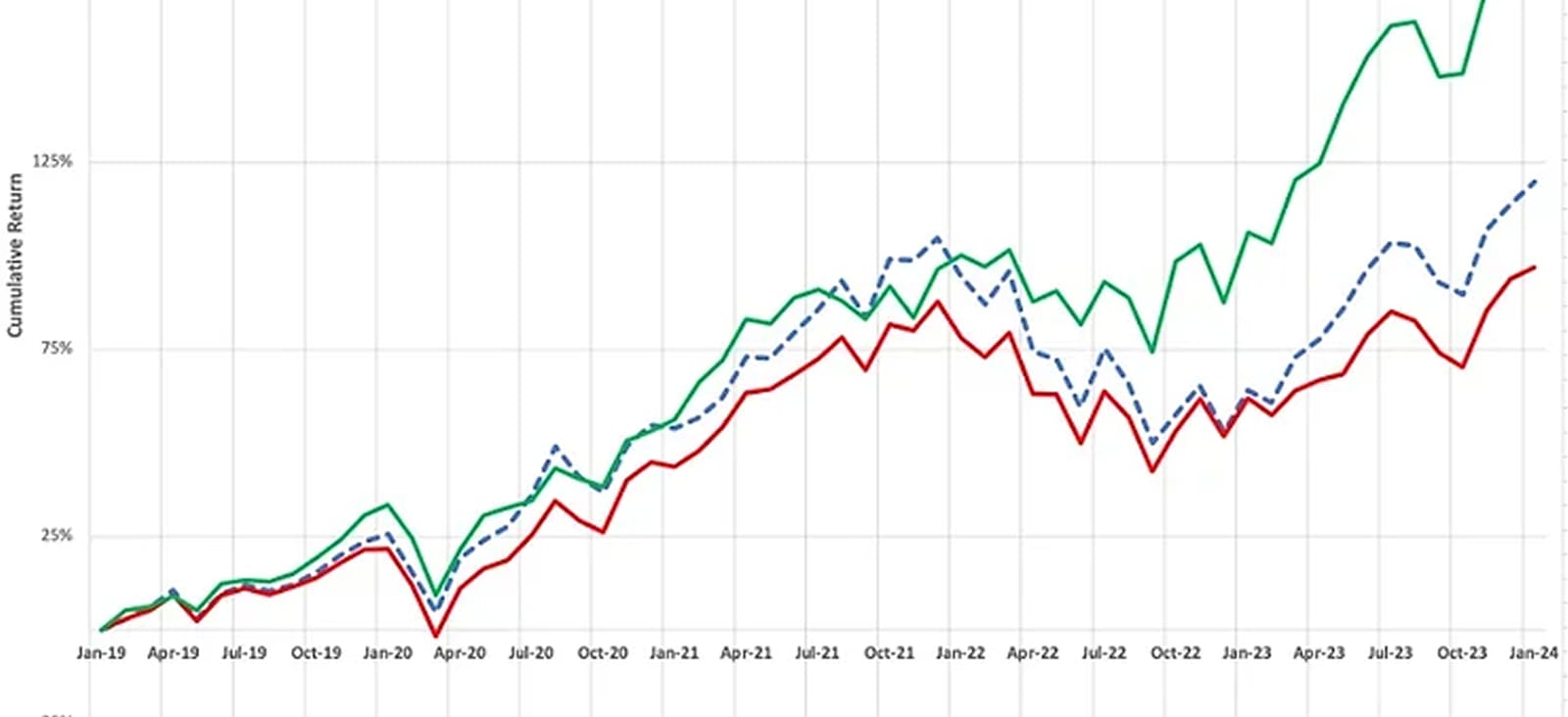

What could be more sensible than buying quality stocks, especially in times of uncertainty? After the tough market of 2022, many argued that a focus on quality stocks would be a good investment approach for 2023, and they were correct.

On January 30, Pensions & Investments reported that a New Hampshire House committee unanimously opposed the proposed bill to make it a felony to knowingly use ESG criteria in investing taxpayer dollars.

The Financial Times published my guest post, 'The quantitative climate change,' in which I highlight a half-century-plus connection between treasury yields and the performance of factor portfolios that quants need to succeed.

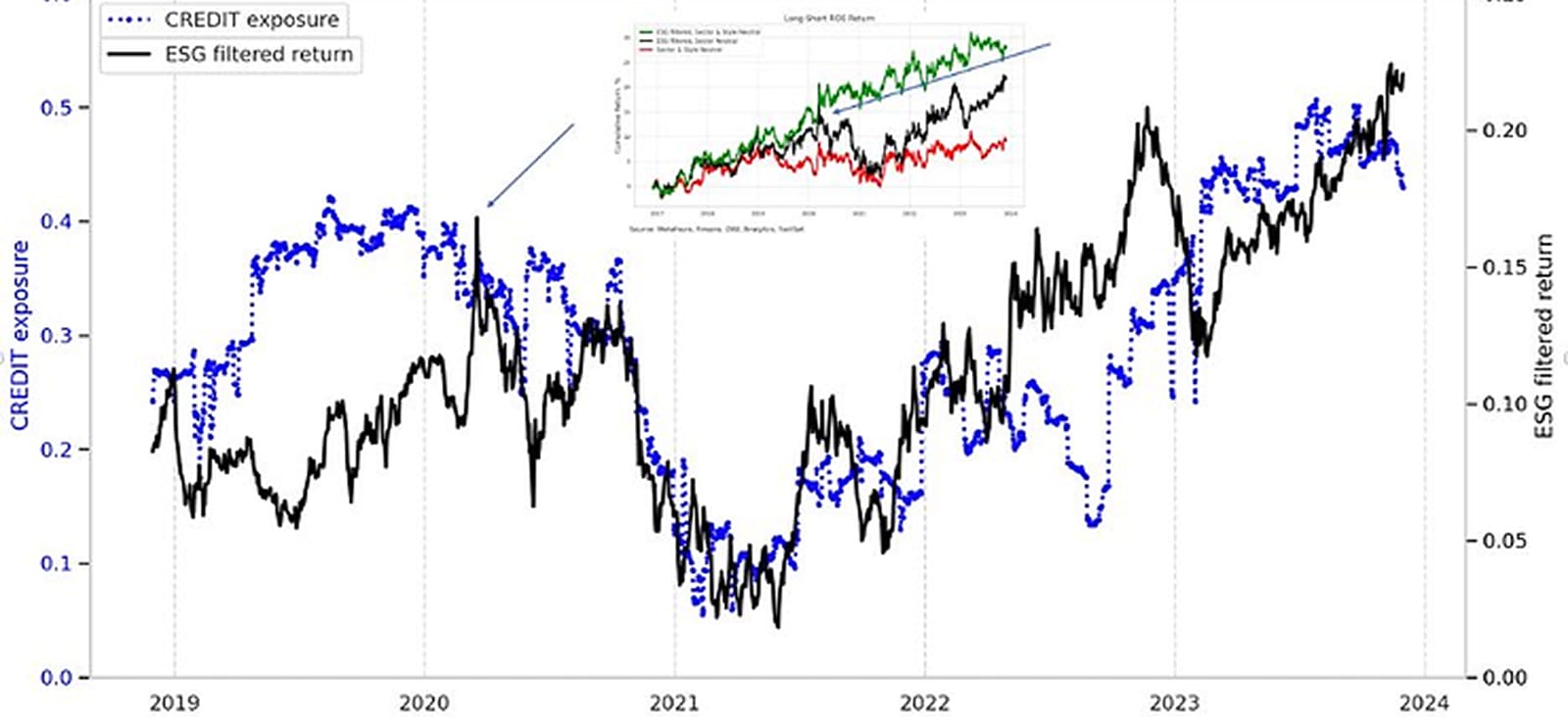

In a previous post, I showed how ESG screening substantially improved a strategy focused on profitability (long-short ROE) that was both sector-neutral and style-neutral. The main point was to reveal the true impact of ESG on equity performance by removing unintended influence.

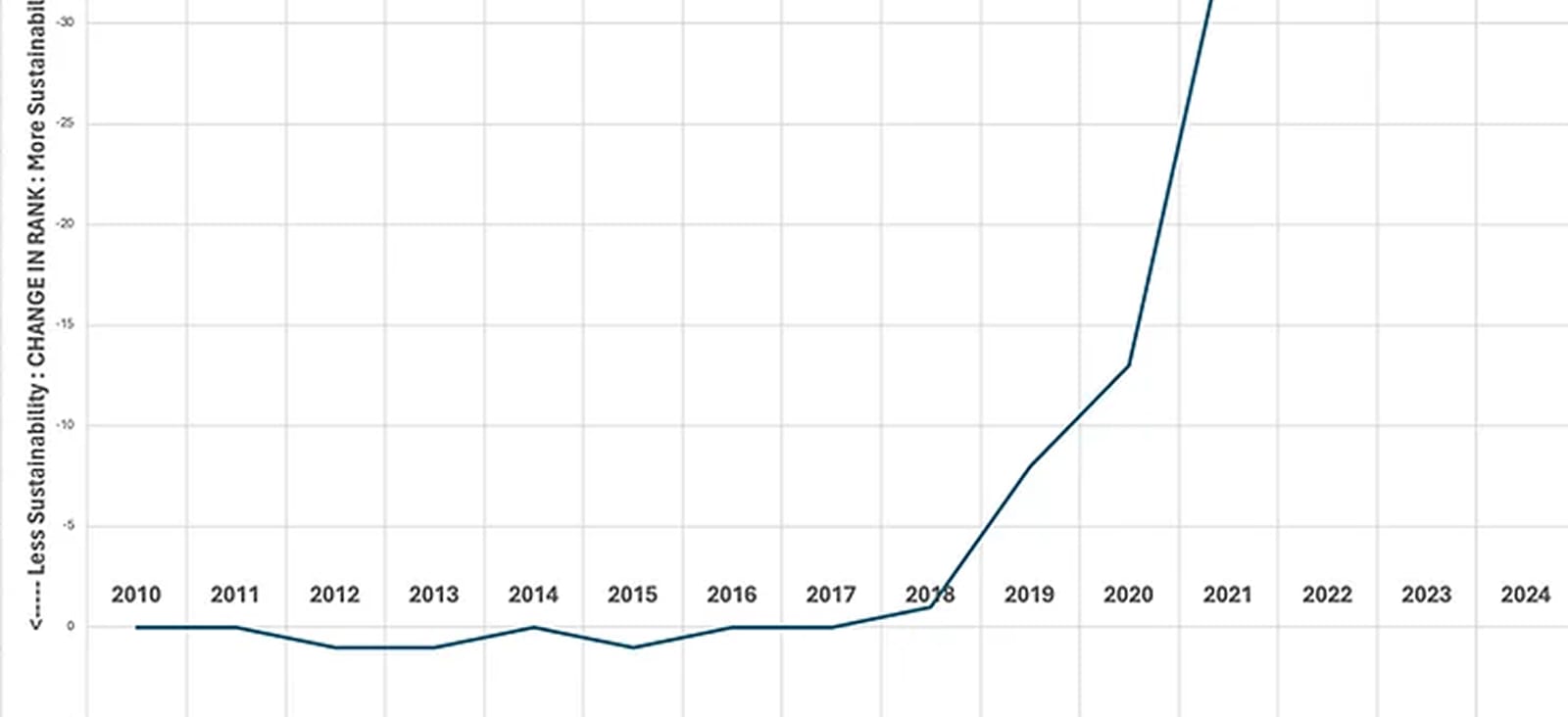

Is there investment value in ESG? It's hard to think of a more polarizing investment topic. Regulators, investors, politicians, and academics have all weighed in. Money has been leaving sustainable funds because of disappointing returns.