In his March State of the Union address, President Biden proposed raising the excise tax on stock buybacks from 1% to 4% to discourage companies from engaging in stock repurchases. On April 12, the Department of Treasury and the IRS followed up with proposed regulations on stock buybacks. Kamala Harris endorses Biden’s plan to quadruple the tax. Is there evidence that the proposed tax has affected buyback-related stock performance? If there was a tax effect, would ongoing stock performance reflect the odds of this tax becoming enacted, reflecting the market’s view of whether Harris or Trump will be the next president?

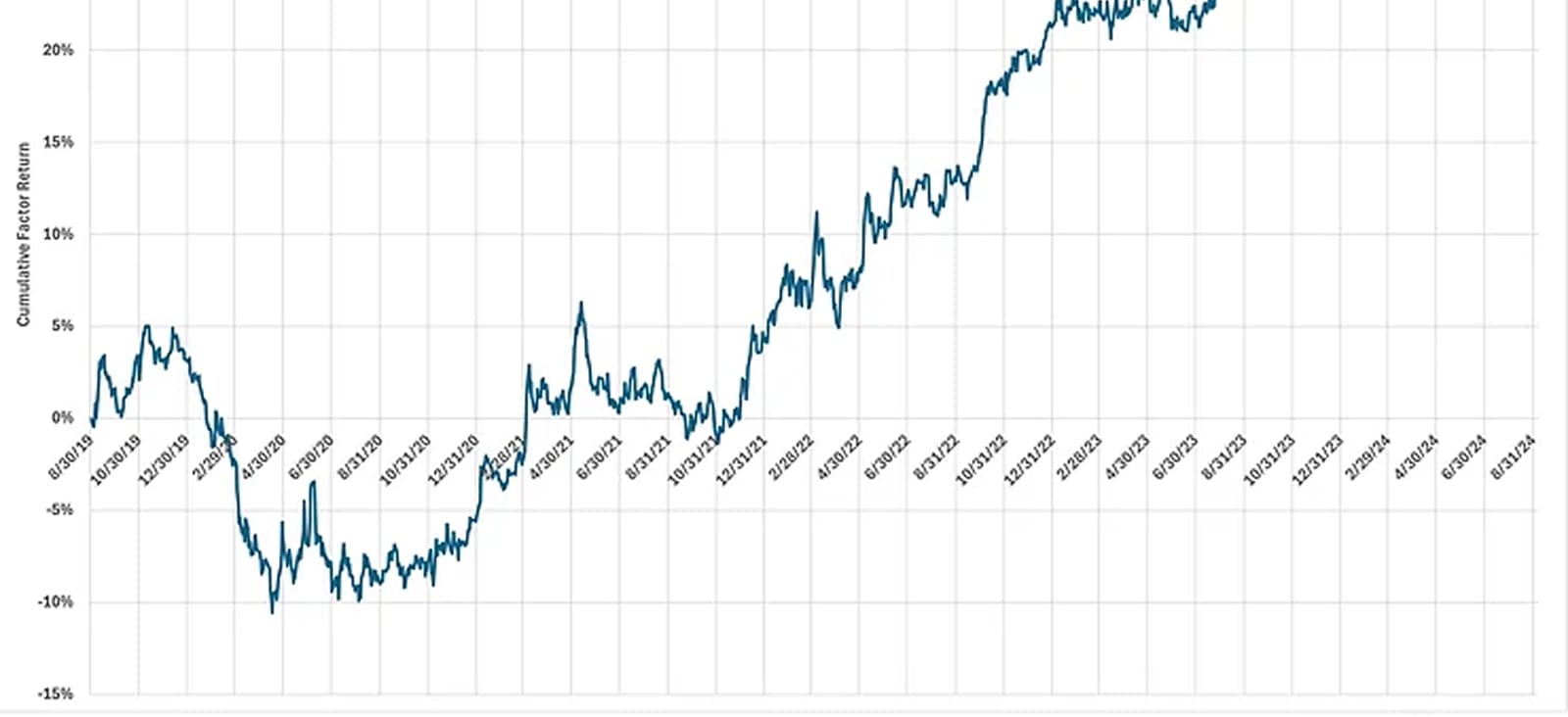

Stock buybacks have been a very good source of factor performance. The chart shows the sector-neutral return of a monthly rebalanced long-short portfolio of S&P 500 stocks, sorted by their one-year relative change in outstanding shares. A share reduction would indicate buybacks, and an increase would indicate share issuance. The chart shows that buybacks as a factor did poorly from mid-December 2019 until mid-April 2020. There was caution about buybacks during the COVID-19 market meltdown.

The return to buybacks bottomed in mid-April 2020 and peaked four years later, in mid-April 2024. Over that period, the buyback cumulative factor return was 29%, with a 1.3 information ratio, outperforming popular strategies like momentum, ROE, Free Cash Flow yield, dividend yield, E/P, etc.

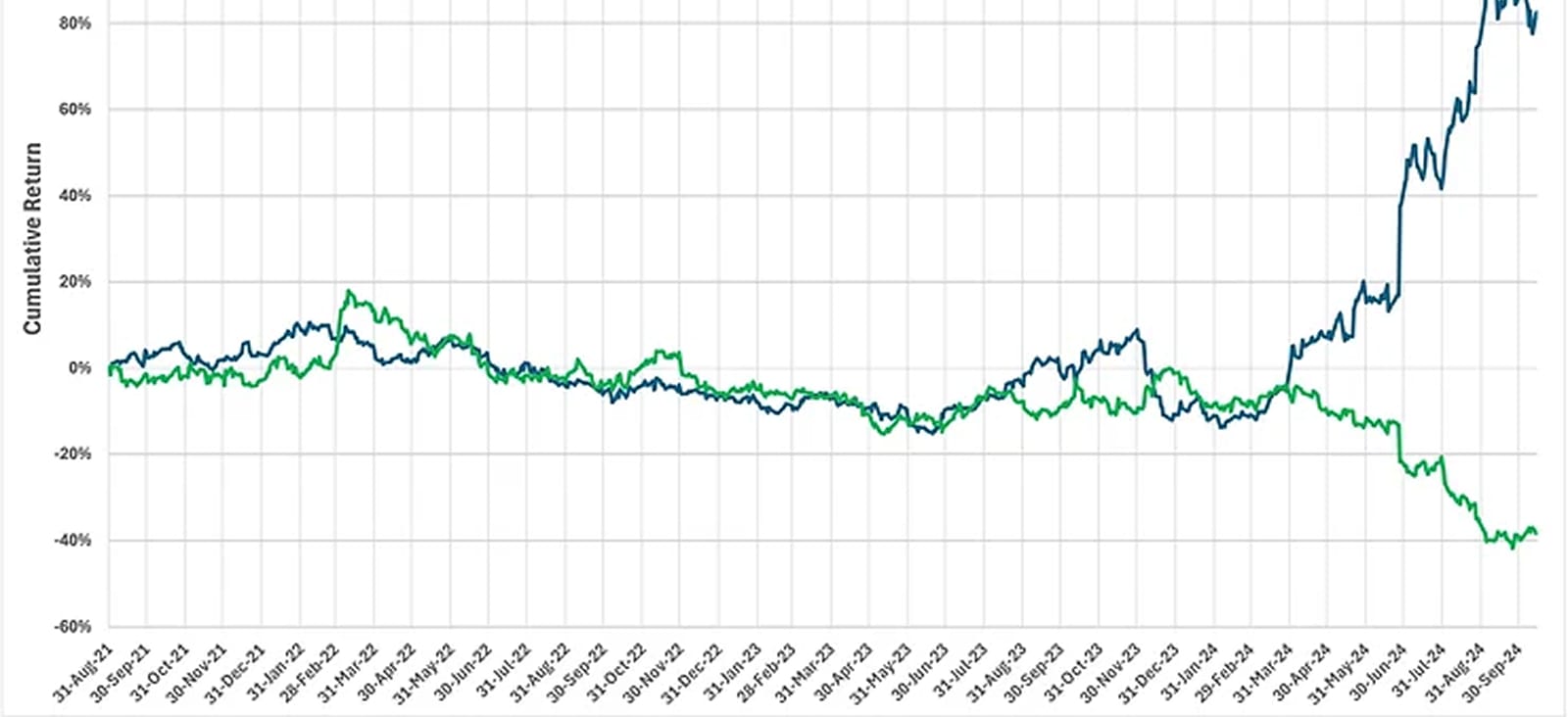

Was the April 2024 peak in buyback returns due to the proposed tax? If that is correct, then the sign of a recovery for the buyback factor returns since July 8, shown in the chart, could be the market’s pricing that the buyback tax increase won’t happen – an election forecast. Or was the buyback peak a sign of caution, something we saw in December 2019? Or perhaps something else? I can’t answer that, but I can say that buybacks should be considered an important source of return and possibly a signal of the market’s pricing of what’s ahead.