Is there investment value in ESG? It's hard to think of a more polarizing investment topic. Regulators, investors, politicians, and academics have all weighed in. Money has been leaving sustainable funds because of disappointing returns.

However, impressions about ESG returns based on ESG funds are flawed because the returns ignore the influence of sectors and investment styles. What is the role of ESG on equity performance if you neutralize the influence of sector and investment style? To answer this, we tested the impact of ESG on profitability, specifically Return on Equity (ROE), as a driver of stock returns.

ROE is a financial metric that is a pillar of quality investing. Is it far-fetched to consider non-financial inputs, such as ESG scores, as indicators of company quality? ESG features such as governance, company transparency, risk management, corruption, and so on can undoubtedly influence investors' opinions on a company's quality. These opinions could affect the reported ROE's impact on the company's stock price. With that in mind, we ran an experiment.

- Produce a long-short portfolio of stocks in the S&P500 that is long the top ROE stocks and short the bottom stocks in each sector. Also, eliminate the style tilts of the sector-neutral portfolios (Finsera risk model).

Produce an ESG-filtered version of this long-short ROE portfolio, using consensus ESG (OWL analytics consensus scores), to include only the top ESG stocks in each sector for the long side and the bottom ESG stocks for the short side.

- Produce a style-neutral version of the ESG-filtered, sector-neutral ROE portfolio.

- Rebalance the long-short portfolios monthly for a seven-year test (starting November 30, 2016).

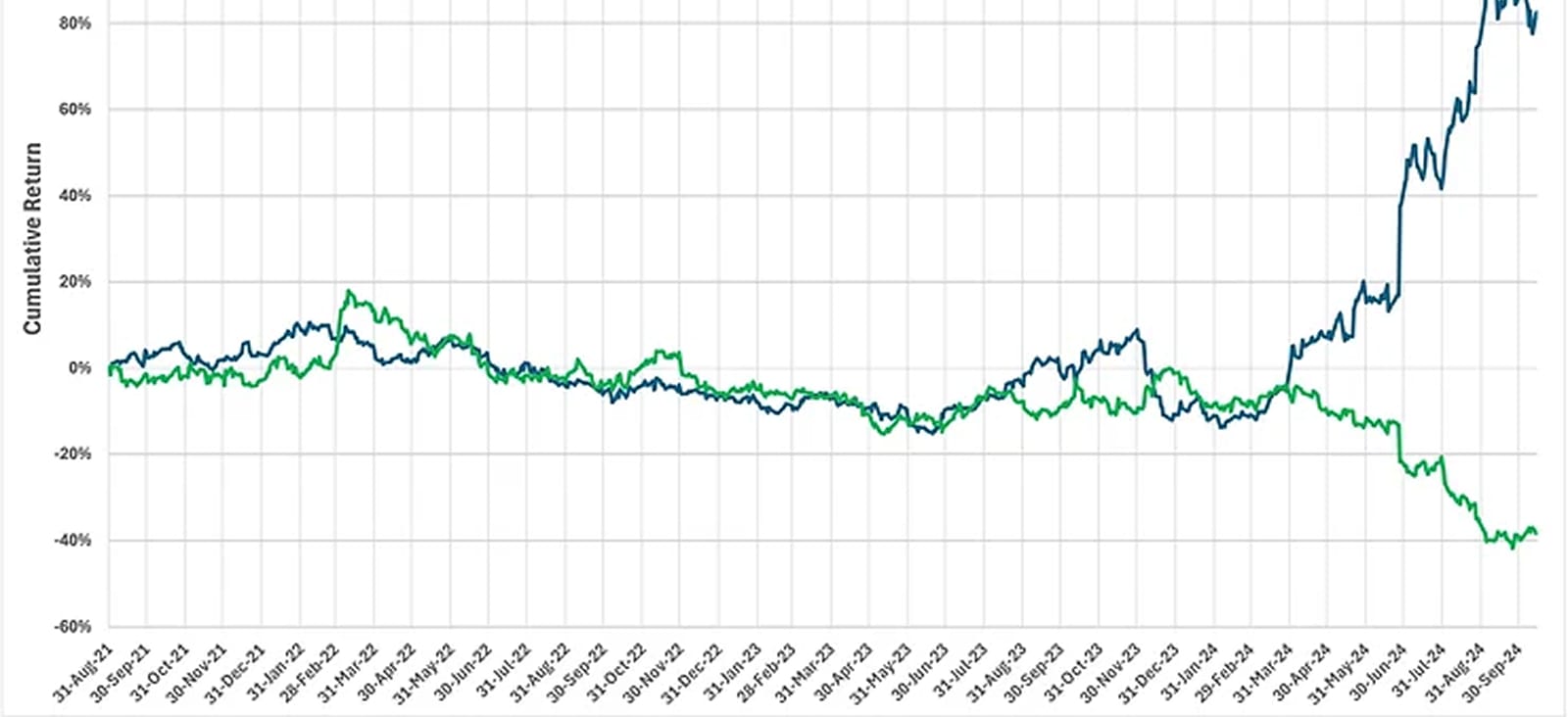

The chart shows the cumulative returns of the three portfolios, revealing the ESG-based performance improvement when you strip away what is masking the ESG signal. Over the seven-year history, the annualized long-short ROE return for S&P500 stocks that is both sector and investment-style neutral was 1.3% (with a 0.3 information ratio). Using consensus ESG scores to filter the long and short stocks while maintaining sector and style neutrality, the return was an annualized 3.6% per year (0.7 information ratio). Using just sector neutrality, without style neutrality, achieved a 2.9% return (0.5 information ratio). The size of the ESG impact is less important than the sign of the impact, which is positive.

Most investors include ESG based on considerations other than improved performance. The pushback to ESG investing is due to an assumed performance cost. Depending on how investors implement strategy and construct portfolios, there can certainly be a cost to ESG. The point made in the chart is that ESG does not require a performance penalty. Stay tuned for follow-up pieces that explore ESG and investment performance.