The sales/employee ratio should be a good measure of employee productivity. However, it varies considerably across market sectors, much higher in capital-intensive industries such as energy and utilities and much lower in more labor-intensive sectors such as industrials and consumer discretionary. The sales/employee ratio has been most effective as a source of investment return in consumer discretionary, a sector that includes retail, hospitality, autos, and entertainment, which rely on large numbers of employees.

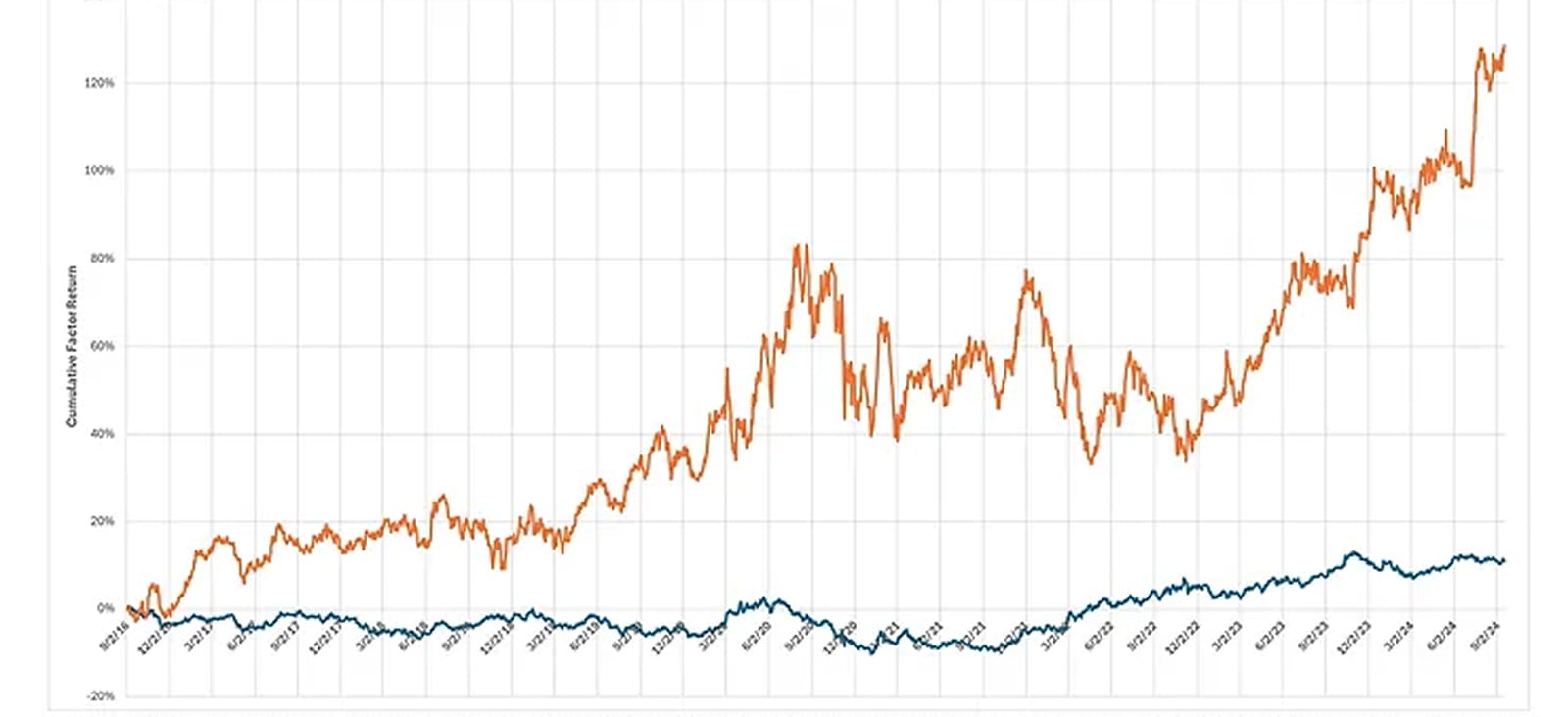

The chart compares the return to sales/employee over the past eight years as a long-short factor in consumer discretionary to the sector-neutral factor return in the S&P500. Over this period, the sales/employee factor in consumer discretionary returned 129% (11% annualized) with a 0.6 information ratio. The S&P500's cumulative factor return for sales/employee over the eight years was 11% (1.3% annualized) with a .24 information ratio. You can see in the chart that the more recent return to productivity in consumer discretionary since the end of 2022 has been more impressive.

Since the end of 2022, the long-short sales/employee factor in consumer discretionary has delivered a 56.7% return (30% annualized) with a 1.9 information ratio. The sector-neutral sales/employee ratio in the S&P500 returned 6.7% (3.9% annualized) with a 0.79 information ratio over the same period.

The market has largely overlooked productivity, as indicated by the sales-per-employee ratio, in most sectors. However, this metric has been a key driver of returns in the consumer discretionary sector, where its impact continues to be significant.