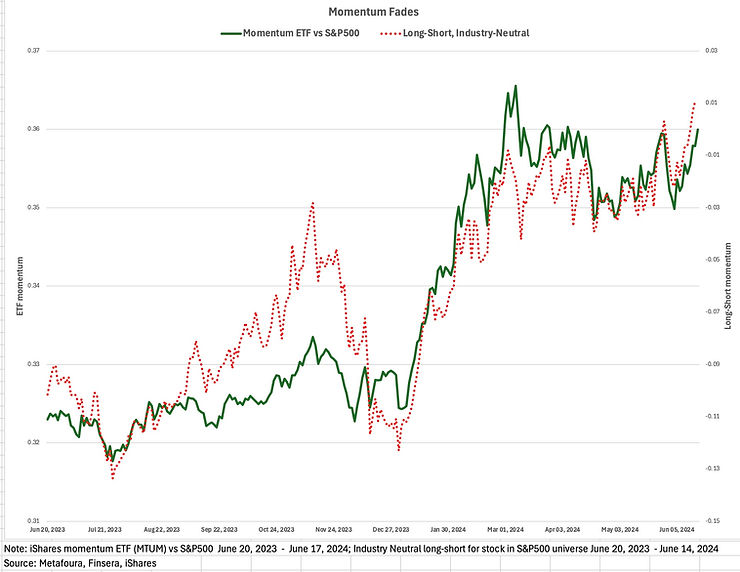

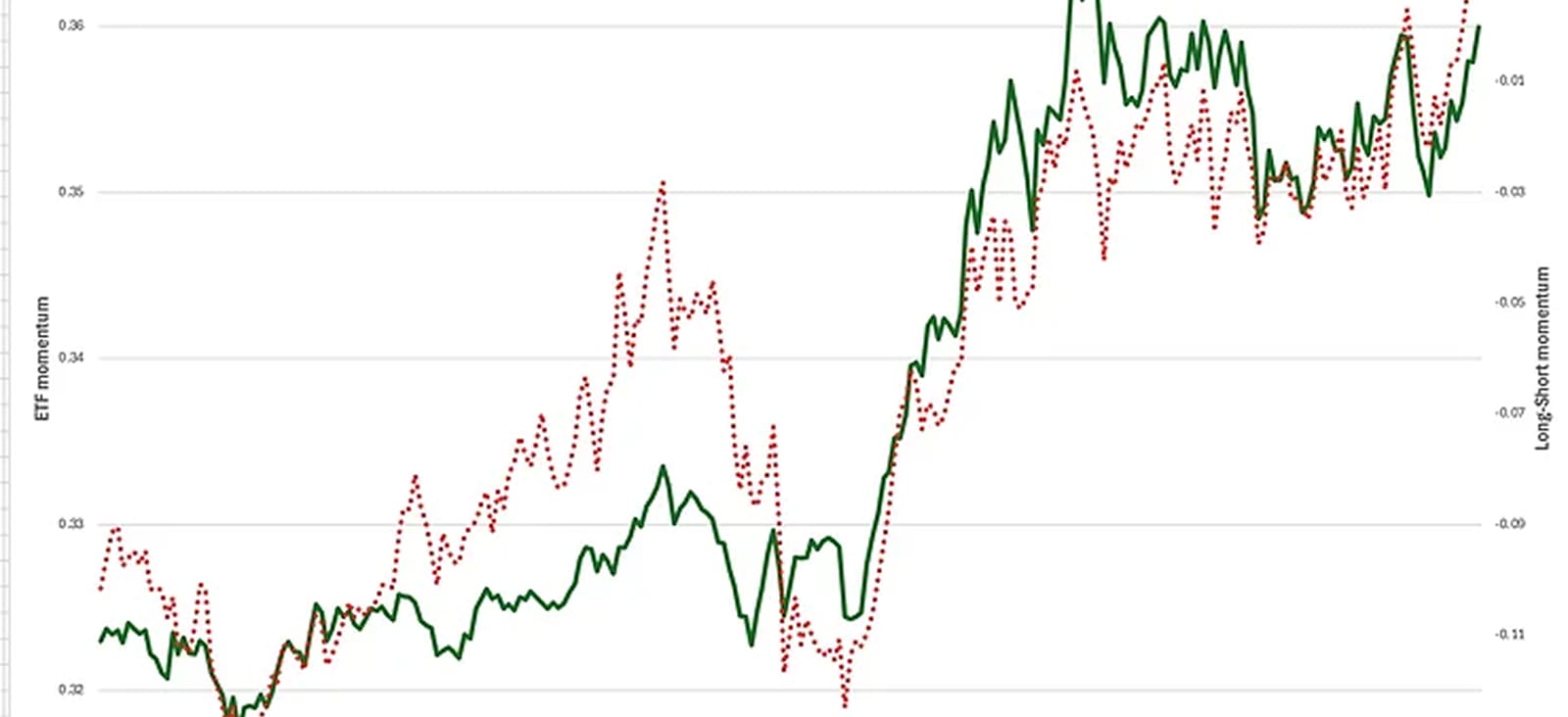

The S&P500 has returned 15% through June 20, 2024. Half of the gains were achieved since early May. Momentum also has a strong 2024, but its excess return this year was achieved before early March. Since then, the power of momentum has spread throughout the market. The chart illustrates the momentum story.

The green line shows the popular iShares momentum ETF's performance relative to the S&P500. This relative performance took off at the start of the year and peaked on March 7. The ETF's flat performance relative to the market since early March probably means that momentum has become pervasive for S&P500 stocks. Hence, an ETF focused on momentum is not a different momentum play than the market. The momentum ETF is designed to focus on the best momentum stocks. But the momentum distinction has faded. There is another way to see that.

The long-short, industry-neutral return for momentum in the S&P500 shown in the chart's red dotted line has also not added value since early March. This loss of added value means there has been negligible dispersion of momentum return across the S&P500 stocks. The tech sector has dominated the excess return of the momentum ETF. The industry-neutral long-short portfolio avoids sector or industry bias and makes a cleaner statement. Momentum is everywhere.